As it is well known, the so-called “mini-budget” of the Chancellor Kwasi Kwarteng, announced on 23 September 2022, has brought forward the biggest tax cut since 1972. The higher rate of income tax (45%, for yearly incomes above £150,000) was removed, effectively lowering it to the second tax rate of 40%, while the basic rate was cut by 1% from 20% to 19%. These changes will take place from April 2023 in all the UK with the exception of Scotland, which has full control over its own tax schedule. Moreover, the new Health and Social Care Levy (HSCL) – increasing the national insurance contribution rate by 1.25 percentage points – was cancelled, with effect from November 2022. Such a drastic reconfiguration of the tax system raises many questions, at a time of high inflation, a large government deficit, and growing economic hardship. Additional measures include a cut in the Stamp Duty, cancelation of a planned hike in corporate tax, further tax reductions for individuals living in investment zones, a freeze of alcohol duties, and extensions of duty-free areas. Together, all these measures will cost the government more than £40 billion in 2023.

Any tax cuts of can appear appealing, especially when household budgets are squeezed by a cost of living crisis. However, tax cuts must be funded. The government is betting on an old economic argument, that lower tax rates can boost investment and growth, and ultimately be self-financing. There are two key problems with this argument. First, there is weak and contradictory evidence in support of this argument; at best it is impossible to say with any certainty that it will work in the UK’s current circumstances, and more likely that the chances of it working are slim. Second, even if the basic economic argument holds, the economic benefits of increased investment and growth require time to take effect; so that it would be best implemented at time of relative stability.

In the short term, the Government’s tax cut can be funded only by reducing spending, increased borrowing, or resorting to the money press. Reducing spending implies cuts in the welfare state, especially when the military budget is ring-fenced due to the war in Ukraine. An increase in borrowing puts the country at the mercy of financial markets. Printing money fuels inflation, and requires an accommodating Central Bank. All of these alternatives appear unpalatable in the current context.

The government has played the card of increased borrowing, with the result of triggering a financial crisis. The Bank of England had to intervene by starting to buy government bonds (that’s the printing press) but the program is time-limited and cannot be extended without further adding to inflationary pressures. If it is not to renege its flagship policy, the government will therefore have to cut welfare provisions, which can be anticipated to extend the distributional consequences observed during the austerity decade of the 2010s into the 2020s.

Nevertheless, in the short term, most people will be happy to see their taxes reduced. The problem is that some people are much happier than others, and our analysis indicates that the people who will benefit most from the planned tax cuts will be the least affected by the looming cuts in welfare. Using UKMOD, the free tax-benefit model for the United Kingdom maintained at the Centre for Microsimulation and Policy Analysis, we have quantified the gains implied by the mini-budget, distinguishing people by their place in the income distribution. Our analysis focuses on the reduction in the basic rate of tax (from 20 to 19%), the abolition of the additional tax rate (for those with income in excess of £150,000 per year), and scrapping of the Health and Social Care Levy, which account for around £25 of the £40 billion projected reduction in revenues. The measures we have not included – from Stamp Duty to corporate taxes – are likely to disproportionately benefit individuals at the top of the income distribution, further strengthening our results.

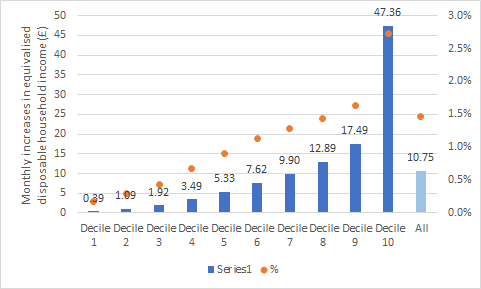

Figure 1 below shows the gains by decile of equivalised household income.

Figure 1: Monthly increases in equivalised disposable household income, 2023, by decile. The baseline is the system before the “mini-budget” announcements.

Note: Blue histogram: nominal changes (left axis). Orange dots: percentage changes (right axis). Source: Our computation using UKMOD version A2.25.

The tax cut will deliver an increase in the household budget to the poorest tenth of the population worth 39 pennies a month, less than one percent of the gains enjoyed by the tenth of the population with the highest private incomes. Even in percentage terms, gains are higher for richer individuals, with the benefit to the highest tenth of the population (2.7%) more than ten times that of the lowest tenth of the population (0.2%).

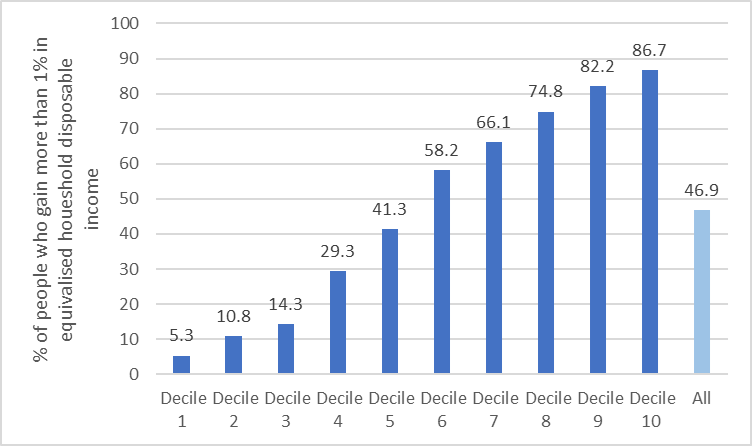

Only 5.3% of the population in that poorest tenth of the population can be expected to gain from the tax cut – with gains defined as an increase in equivalised disposable household income worth at least than 1 percentage point. On the other hand, more than 85% of individuals in the richest decile are set to gain from the reforms (Figure 2). And “big” gains worth 5% or more are found only among the tenth of the population with the highest incomes (8.5% of the decile).

Figure 2: Gainers (more than 1% of equivalised disposable household income), 2023, by decile. The baseline is the system before the “mini-budget” announcements.

Source: Our computation using UKMOD version A2.25.

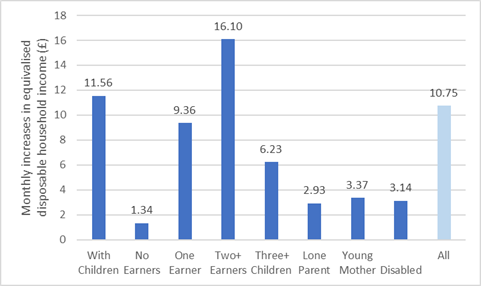

Not surprisingly, more vulnerable groups – no earners, lone parents, young mothers and disabled – are unlikely to gain much from the reform (Figure 3). The elderly are also expected to achieve “mini-gains” from the “mini-budget”, with an increase in equivalised monthly disposable household income of only three pounds and twenty pennies, on average (result not shown in the figure).

Figure 3: Monthly increases in equivalised disposable household income, 2023, by household type. The baseline is the system before the “mini-budget” announcements.

Source: Our computation using UKMOD version A2.25.

In conclusion, our analysis confirms that the tax cut is highly regressive. Short term effects see winners concentrated mostly amongst the richest part of the UK population. Long-term gains for the UK economy are dubious to say the least. With borrowing becoming increasingly expensive, and the lifeline provided by the Bank of England unsustainably in the medium term, the only path ahead appears to be one of welfare retrenchment, more austerity, and reduced public services.

More hardship for most, to increase advantage for the few: The UK is imparting to the world a lesson in bad economic management.

+++

PS> Since we published our analysis, the Chancellor has announced a U-turn on the abolition of the 45% higher rate of income tax. We show here that this doesn’t radically change the regressive nature of the package.